How to Resist Impulse Buying: Master Your Spending Decisions

Impulse spending feels harmless in the moment but it can quietly wreck your budget on a bigger scale than most people realize. Nearly 90 percent of Americans admit to making impulse purchases each year. Most believe it’s only a matter of weak willpower or flashy sales offers. Turns out, the real driver is your emotional state and environment, and understanding those hidden triggers is the first step to taking back control of your wallet. Table of Contents * Step 1: Identify Your Triggers For

Impulse spending feels harmless in the moment but it can quietly wreck your budget on a bigger scale than most people realize. Nearly 90 percent of Americans admit to making impulse purchases each year. Most believe it’s only a matter of weak willpower or flashy sales offers. Turns out, the real driver is your emotional state and environment, and understanding those hidden triggers is the first step to taking back control of your wallet.

Table of Contents

- Step 1: Identify Your Triggers For Impulse Buying

- Step 2: Create A Budget And Set Spending Limits

- Step 3: Develop A Wishlist For Future Purchases

- Step 4: Pause And Reflect Before Making A Purchase

- Step 5: Practice Mindful Shopping Strategies

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Identify Your Impulse Triggers | Recognize emotional and environmental cues that lead to unplanned purchases for better self-control. |

| 2. Create a Concrete Budget | Structure your income and expenses to set intentional spending limits that allow for mindful consumption. |

| 3. Develop a Strategic Wishlist | Use a wishlist to postpone impulse buying and assess future purchases against financial goals. |

| 4. Implement a Reflection Process | Pause before purchases to evaluate needs versus wants, helping curb impulsive behavior. |

| 5. Practice Mindful Shopping Techniques | Adopt strategies that encourage deliberate spending, focusing on long-term financial health and well-being. |

Step 1: Identify Your Triggers for Impulse Buying

Understanding your personal impulse buying triggers is the critical first step in mastering financial self-control. These triggers are the psychological and environmental cues that push you toward making unplanned purchases, often driven by emotions, marketing strategies, or personal vulnerabilities.

Understanding Emotional and Environmental Triggers

Impulse buying rarely happens by accident. Your spending behaviors are typically rooted in specific emotional states and external stimuli. Some people shop when feeling stressed, lonely, or seeking temporary happiness. Others get tempted by strategic retail environments designed to provoke spontaneous purchases. According to research from the National Institutes of Health, both internal psychological factors and external environmental cues significantly influence purchasing decisions.

To effectively identify your triggers, start by creating a detailed spending journal. Document not just what you buy, but your emotional state, location, and circumstances surrounding each unplanned purchase. Track patterns like late-night online shopping when feeling tired, browsing social media during work breaks, or wandering through mall stores when bored. Notice if certain environments like sale events, targeted advertisements, or specific websites consistently lead you to impulse purchases.

Recognize common trigger categories that might prompt unnecessary spending:

- Emotional triggers: Stress, boredom, celebration, sadness

- Social media influence: Targeted ads, influencer promotions

- Retail environment strategies: Limited time offers, visual merchandising

- Personal vulnerabilities: Low self-esteem, seeking instant gratification

Once you map these triggers, you gain powerful self-awareness. This understanding allows you to develop proactive strategies for redirecting your spending impulses before they transform into actual purchases.

Below is a table summarizing common impulse buying triggers and examples from the article, helping you recognize which cues may influence your own spending decisions.

| Trigger Category | Description | Example from Article |

|---|---|---|

| Emotional Triggers | Feelings that drive spontaneous purchases | Stress, boredom, celebration, sadness |

| Social Media Influence | Exposure to targeted advertising or influencer content | Targeted ads, influencer promotions |

| Retail Environment Strategies | In-store or online tactics designed to prompt quick buys | Limited time offers, visual merchandising |

| Personal Vulnerabilities | Individual tendencies or needs impacting spending | Low self-esteem, seeking instant gratification |

| Environmental Cues | Situational factors in your surroundings | Browsing during work breaks, late-night online shopping |

Remember, identifying triggers is not about self-judgment but building practical financial awareness. By understanding your unique spending psychology, you create the foundation for more intentional and controlled purchasing decisions.

Step 2: Create a Budget and Set Spending Limits

Establishing a clear budget is your strategic blueprint for controlling impulse buying and transforming your financial behavior. This step transforms abstract spending intentions into concrete, actionable financial guidelines that protect your wallet and empower your decision making.

Start by conducting a comprehensive financial inventory of your current income and expenses. Track every dollar you earn and spend for one complete month, using digital tools like spreadsheet apps or dedicated budgeting platforms. According to research from the University of Michigan, implementing a structured approach to monitoring spending significantly reduces impulsive purchase tendencies.

Break down your monthly income into critical categories: essential expenses (housing, utilities, groceries), savings goals, debt repayment, and discretionary spending. The key is creating intentional spending limits that feel sustainable, not restrictive. Financial experts recommend the 50/30/20 rule: 50% for necessities, 30% for personal wants, and 20% toward savings and debt reduction.

To effectively curb impulse buying, establish specific subcategories within your discretionary spending allocation. Create a dedicated “discretionary fund” with a strict monthly limit that covers entertainment, dining out, clothing, and spontaneous purchases. This approach transforms your spending from an emotional reaction to a planned, thoughtful decision.

Implement practical strategies to enforce your budget:

- Use cash envelopes for discretionary spending categories

- Set up automatic transfers to savings accounts

- Utilize mobile banking apps with real-time spending alerts

- Delete saved payment information from online shopping platforms

Explore our guide on personalized shopping experiences to further refine your financial strategy. The goal isn’t complete deprivation but mindful, intentional spending that aligns with your long-term financial goals.

Verify your budget’s effectiveness by reviewing your spending weekly. Track how closely you adhere to predetermined limits, making adjustments as needed. Success isn’t perfection but consistent improvement in your financial decision-making process.

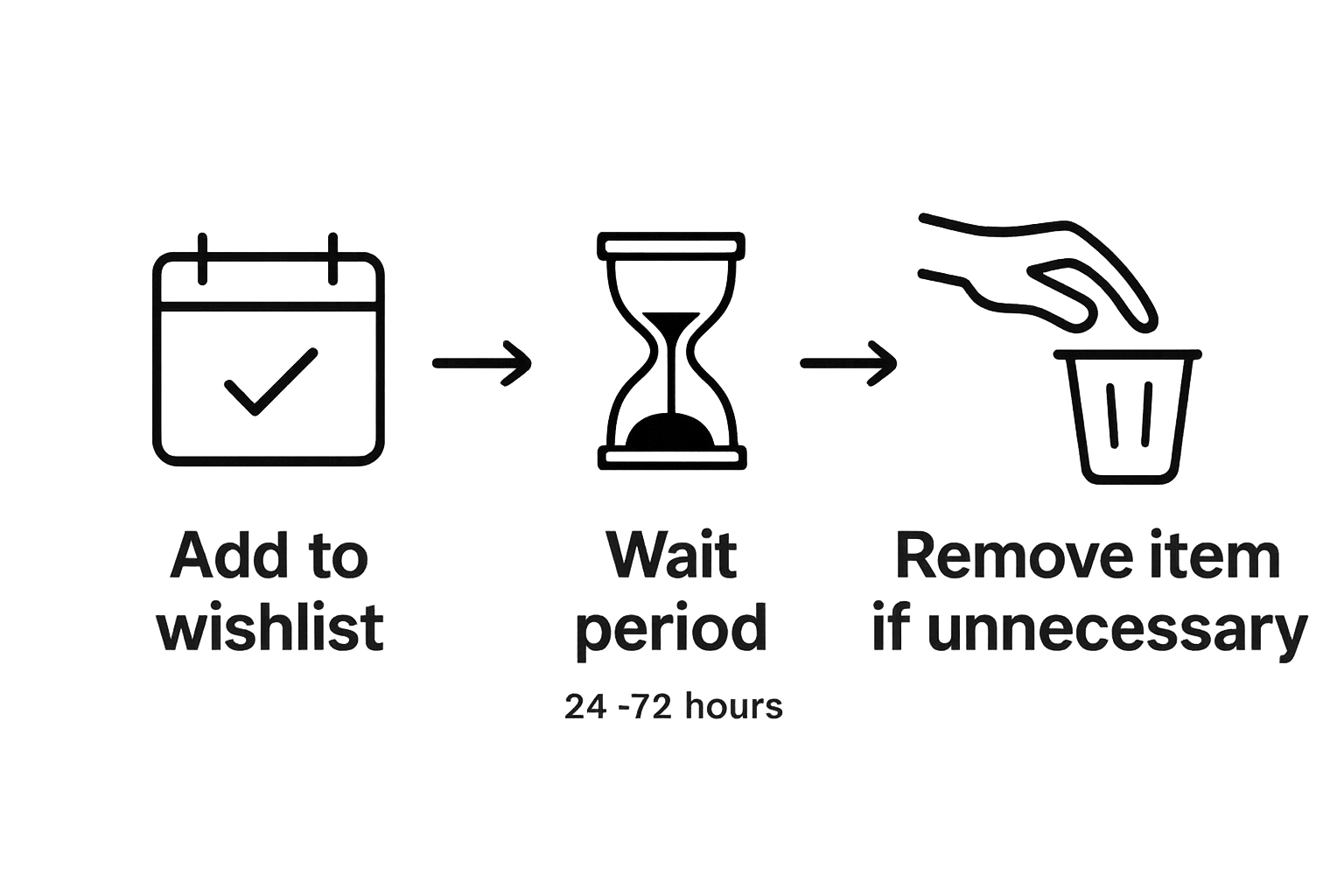

Step 3: Develop a Wishlist for Future Purchases

Transforming impulse buying into intentional purchasing begins with creating a strategic wishlist that serves as a powerful financial management tool. This step moves you from reactive spending to proactive planning, giving your financial desires structure and purpose.

A well-designed wishlist acts as a psychological buffer between desire and purchase, allowing you to evaluate potential acquisitions critically. According to research from the National Institutes of Health, implementing a cooling-off period through written lists can dramatically reduce impulsive buying behaviors.

Start by establishing digital or physical wishlist platforms that support thoughtful curation. Use specialized apps or learn about comprehensive wishlist management techniques that help track potential purchases systematically. When you encounter something tempting, immediately add it to your list instead of buying immediately. Include critical details like item price, potential utility, and how the purchase aligns with your broader financial goals.

Develop a robust evaluation process for items on your wishlist. Each potential purchase should pass a series of strategic questions: Do I genuinely need this? Can I afford it without disrupting my budget? Will this item provide long-term value or satisfaction? Implement a mandatory waiting period typically ranging from 24 to 72 hours before considering any wishlist item for purchase. This pause allows emotional impulses to subside and rational decision-making to emerge.

Create wishlist categories that reflect your financial priorities:

- Essential future needs

- Personal development investments

- Meaningful experiences

- Long-term goal-related purchases

- Potential gift items

Regularly review and prune your wishlist, removing items that no longer align with your current financial situation or personal objectives. This maintenance keeps your list dynamic and meaningful.

Some items might remain on the list for months, while others will be quickly discarded, demonstrating your growing financial discipline.

Successful wishlist management means transforming your relationship with spending. It’s not about restricting yourself but about making intentional, well-considered purchasing decisions that genuinely enhance your life and support your financial well-being.

Step 4: Pause and Reflect Before Making a Purchase

The moment before purchasing represents a critical decision point where impulse meets intention. Developing a deliberate pause and reflection process transforms your buying behavior from reactive spending to mindful consumption. This step is about creating mental space between desire and action, allowing rational thinking to override emotional impulses.

Implementing a structured reflection protocol becomes your financial defense mechanism. When an item catches your eye, immediately activate a personal purchasing pause sequence. Start by physically stepping away from the product or closing the online shopping tab. Take three deep breaths and ask yourself a series of strategic questions that challenge the immediate desire to purchase.

Design a personal reflection checklist that interrogates your potential purchase from multiple angles. Consider questions like: Will this item genuinely improve my life? Do I already own something similar? Can I afford this without disrupting my budget? How many hours of work would I need to invest to purchase this item? Quantifying purchases in terms of labor hours often provides startling perspective.

Technology can be an incredible ally in your reflection process. Use smartphone apps or digital timers to enforce mandatory waiting periods. Some individuals find success with 24-hour, 48-hour, or even week-long cooling periods before making non-essential purchases. Learn more about creating personalized shopping experiences that align with your financial goals and emotional well-being.

Develop reflection strategies that work with your personal psychology:

- Create a pros and cons list for each potential purchase

- Screenshot or photograph items instead of buying immediately

- Share potential purchases with a financially responsible friend

- Calculate the item’s cost in terms of hours worked

- Visualize the item’s long-term utility

Remember that reflection is not about deprivation but about making intentional choices. Some purchases will pass your reflection test and represent genuine value. Others will reveal themselves as fleeting desires that do not merit your hard-earned resources. The goal is building a thoughtful relationship with spending that prioritizes your long-term financial health and personal satisfaction.

Successful reflection means consistently choosing financial wisdom over momentary gratification. Each paused purchase is a small victory in your journey toward mindful consumption.

The table below offers practical reflection strategies mentioned in the article that you can use to pause and better evaluate your purchases before completing them.

| Reflection Strategy | How It Works | Purpose |

|---|---|---|

| Pros and Cons List | Write out advantages and disadvantages | Objectively assess if the purchase is worthwhile |

| Screenshot or Photograph Items | Capture items visually without buying immediately | Create space for delayed decision-making |

| Share with a Responsible Friend | Discuss your intended purchase with someone trusted | Gain outside perspective and accountability |

| Calculate Cost in Labor Hours | Convert price to the number of work hours required | Contextualize the true value and effort involved |

| Mandatory Waiting Period (Timer/App) | Use technology to set a delay before purchasing | Allow emotions to subside and reduce impulsivity |

| Visualize Long-Term Utility | Imagine how the item will serve you over time | Clarify actual long-term value and usefulness |

Step 5: Practice Mindful Shopping Strategies

Mindful shopping transforms consumption from an unconscious habit into an intentional, strategic process. This step is about developing a comprehensive approach that shifts your relationship with spending from reactive impulse to deliberate choice, creating sustainable financial habits that protect your wallet and emotional well-being.

Mindfulness in shopping begins with understanding your psychological triggers and creating deliberate intervention strategies. According to research from the CHI Conference on Human Factors, successful impulse buying prevention involves reflection, spending limits, and strategic postponement. Implement these principles by developing a personal shopping protocol that interrupts automatic purchasing behaviors.

Start by redesigning your shopping environment to minimize temptation. Unsubscribe from marketing emails, remove saved payment information from online platforms, and create physical and digital barriers between yourself and potential impulse purchases. Explore budget-friendly shopping approaches that help you make more intentional purchasing decisions without feeling restricted.

Develop a comprehensive mindful shopping toolkit that transforms your purchasing approach. This includes creating visual reminders of your financial goals, practicing gratitude for existing possessions, and consistently asking yourself critical questions before any purchase. Visualize the long-term implications of each buying decision, considering not just immediate gratification but future financial impact.

Establish practical mindful shopping strategies:

- Use cash or prepaid cards with strict spending limits

- Photograph items instead of purchasing immediately

- Wait 24-48 hours before completing any non-essential purchase

- Track emotional states during shopping experiences

- Calculate purchases in terms of work hours required to afford them

Recognize that mindful shopping is a skill developed through consistent practice. Some days will be more challenging than others, and occasional slip-ups are part of the learning process. The goal is progressive improvement, not absolute perfection. Each mindful decision represents a small victory in reclaiming control over your financial choices.

Successful mindful shopping means developing a deep understanding of the difference between wants and needs. It’s about creating a harmonious relationship with consumption that aligns with your personal values, financial goals, and long-term well-being.

Transform Impulse Control Into Powerful Wishlist Planning

Are you tired of emotional spending and regretful purchases? The real challenge is not just recognizing impulse buying triggers or creating budgets, but also having a practical way to pause and reflect before you spend. In the article, you have learned how pausing, wishlisting, and mindful strategies build intentional spending habits. Now, take this a step further with LMK.today. Imagine instantly capturing products from any online store as you browse. Instead of giving in to the urge to buy, save those tempting finds to your personal wishlist and revisit them only when it fits your goals and budget.

Start using LMK.today to build your own intentional wishlist collections. Organize future purchases, track discounts in real-time, and invite friends or family to help you stay on budget for special events. Want to learn more about creating goal-driven, organized shopping experiences? Dive into what is a wishlist and its benefits or see how to share your wishlist to stay accountable. Skip regret and take control of your spending journey today with LMK.today.

Frequently Asked Questions

What are the main triggers for impulse buying?

Impulse buying triggers can be emotional, such as stress or boredom, and environmental, including marketing strategies or retail atmosphere. Recognizing these triggers helps you manage your spending.

How can I create a budget to control impulse buying?

To create a budget, begin by tracking your income and expenses for a month. Allocate funds for essentials, savings, and discretionary spending, using methods like the 50/30/20 rule to set sustainable spending limits.

What is a wishlist and how can it help prevent impulse buying?

A wishlist is a list of desired items that you create before deciding to purchase. It allows you to evaluate needs and prioritize purchases, reducing the likelihood of impulse buying by promoting thoughtful consideration before spending.

What strategies can I use to practice mindful shopping?

Mindful shopping strategies include pausing before making a purchase, redesigning your shopping environment to minimize temptation, using cash or prepaid cards to limit spending, and reflecting on your emotional state during shopping to separate needs from wants.

Recommended

Ready to create your wishlist?

Start building beautiful wishlists that work everywhere.